Liquidity ratios are crucial financial metrics that assess a company’s ability to meet its short-term obligations using its current assets. These ratios, including the current ratio, quick ratio, and cash ratio, provide insights into a company’s financial health and stability. Higher liquidity ratios generally indicate a stronger ability to cover debts and manage unexpected expenses.

While the current ratio considers all current assets, the quick ratio excludes inventory for a stricter measure, and the cash ratio focuses solely on cash and cash equivalents. Investors and analysts use these ratios to evaluate financial risk and make informed decisions. However, it’s important to note that ideal liquidity ratio benchmarks can vary across industries, reflecting different operational needs and asset structures.

Liquidity ratios measure how effectively a company or bank can pay its short-term debts. These ratios examine property, like cash and receivables, to liabilities. The intention is to see if there’s enough cash to fulfill payments whilst they are due. Higher liquidity ratios display the employer can easily repay debts. Lower ratios mean it’d struggle to achieve this. Common liquidity ratios encompass the modern-day ratio, brief ratio, and cash ratio.

Each ratio specializes in exceptional components of an organization’s balance sheet, like contemporary assets or cash reachable. These ratios are vital for agencies due to the fact they show how stable and stable the corporation is. Banks and agencies use these ratios to manage chances and avoid problems.

Liquidity ratios help investors, lenders, and executives apprehend economic health. Strong liquidity lowers the risk of failure during challenging times, ensuring that short-term obligations are met. Having top liquidity means the organization or financial institution can meet its brief-term obligations.

Not sure how to apply liquidity ratios in your financial evaluations? Our experts at capitalizethings.com can guide you step-by-step. Call us on +1 (323)-456-9123 or reach out through by emailing us for your free 15-minute consultation to get started.

What Is Meant By Liquidity?

Liquidity in accounting refers to how quickly a company can pay its short-term debts. It looks at how fast assets can be turned into cash to cover current liabilities. Liquidity ratios use probabilities to expose if a commercial enterprise will pay off debts when they fall due. Companies with high liquidity can meet brief-time period responsibilities. Debtors sense greater steady lending to organizations that have strong liquidity. Companies that can not pay debts when due might face extreme problems.

Businesses need to manipulate liquidity cautiously to avoid danger. Liquidity suggests the general fitness of the business enterprise’s finances. Current liabilities want to be watched to make certain payments are made on time. When debts are due, strong liquidity ensures they’re paid without issues. The excellent businesses control liquidity carefully to avoid shortfalls. Liquidity is important to strolling an enterprise efficiently.

What Is Liquidity In Banking?

Liquidity in banking measureshow much cash and liquid assets a bank has to meet its obligations. Banks need cash to pay depositors, meet prices, and manipulate loans. Liquidity helps avoid the risk of a financial institution run, in which depositors pull out money fast. Banking regulators want banks to preserve liquidity for protection. Liquid property in banking encompasses cash, income from loans, and forecasted credit score traces.

Without liquidity, a bank risks walking out of cash, harming depositors. Interest rates impact liquidity by way of affecting how much income the bank earns. Banks keep a near eye on liquidity to keep away from crumble. Forecasts assist banks in the event that they have enough cash to pay responsibilities. Banks that lack liquidity ought to face issues with depositors and regulators. Keeping excessive liquidity enables banks to construct consideration with depositors and lenders. Managing liquidity reduces the risk of sudden problems.

How To Interpret Liquidity Ratios?

Liquidity ratios indicate a company’s or bank’s ability to cover short-term debts. The present day ratio suggests how properly current assets cover liabilities. An excessive ratio manners strong liquidity, at the same time as a low ratio indicators danger. The quick ratio seems at the capacity to pay debts without counting on inventory. It is stricter than the current ratio.

The cash ratio specializes in cash and near-cash assets to see how without problems an organization pays its debts. Interpreting these ratios allows companies to recognize their financial function. A higher liquidity ratio is a sign of safety. Lower ratios can warn of monetary trouble in advance.

Companies and banks want to reveal liquidity ratios frequently to keep away from cash shortages. Investors and creditors additionally watch those ratios to decide if an organization or bank is strong. Good liquidity control continues a business or bank secure from unexpected charges or dangers.

What Is A Liquidity Ratio For Dummies?

A liquidity ratio for dummies shows how clean it is for an employer to pay its money owed. It compares what the corporation owns (like cash) to what it owes (like payments). If the ratio is excessive, the organization pays its bills without problems. If it’s far lower, the company will have problems paying its payments.

There are 3 principal liquidity ratios: the contemporary ratio, the fast ratio, and the cash ratio. The modern ratio seems in any respect assets. The short ratio ignores stock. The cash ratio only seems to be cash. These ratios help organizations know if they are able to hold running easily. An excellent liquidity ratio helps avoid threats. It tells companies if they have sufficient cash to live securely. Investors and lenders use those ratios to look if an agency is solid. Companies need to control their liquidity properly to avoid cash problems.

How To Find The Liquidity Ratio?

To find the liquidity ratio, compare a company’s current assets to its current liabilities. The method relies upon a sort of liquidity ratio. For the contemporary ratio, divide cutting-edge assets by current liabilities. For the fast ratio, subtract inventory from contemporary property, then divide by contemporary liabilities. For the cash ratio, divide cash and equivalents by way of modern liabilities.

The end result tells how well an enterprise can meet its short-term duties. A better ratio indicates better liquidity. A lower ratio ought to indicate economic hassle. Liquidity ratios assist companies, banks, and buyers recognize monetary fitness. They show if a commercial enterprise will pay its money owed when they’re due. Keeping a robust liquidity ratio enables organizations to keep away from risk and hold balance. It is critical to calculate liquidity ratios regularly to stay on top of financial conditions.

For businesses struggling to analyze their liquidity ratio, we offer expert advice at capitalizethings.com. Reach out or call +1 (323)-456-9123 before using the number and enjoy a free 15-minute consultation to discuss how our services can boost your financial planning efforts.

What Are The Different Types Of Liquidity Ratios?

20 types of liquidity ratios are:

Current Ratio: Measures the capacity to pay short-term responsibilities with modern-day assets.

Quick Ratio (Acid-Test Ratio): Excludes stock from current belongings for a stricter measure of liquidity.

Cash Ratio: Evaluates the ability to pay short-term money owed the usage of cash and cash equivalents.

Operating Cash Flow Ratio: Assesses liquidity with the aid of comparing running cash go with the flow to liabilities.

Current Liability Coverage Ratio: Compares operating income to contemporary liabilities.

Net Working Capital Ratio: Evaluates internet operating capital to present day liabilities.

Interest Coverage Ratio: Assesses a company’s capacity to pay interest on remarkable debt.

Debt-to-Equity Ratio: Measures total debt in opposition to shareholders’ rights.

Debt Ratio: Compares general liabilities to total belongings.

Cash Flow Coverage Ratio: Evaluates how well cash drift covers debt bills.

Cash Conversion Cycle: Measures how quickly a business enterprise can convert investments into cash.

Accounts Payable Turnover Ratio: Evaluates how fast an agency pays off providers.

Accounts Receivable Turnover Ratio: Assesses how speedy receivables are collected.

Inventory Turnover Ratio: Measures how fast stock is sold.

Sales to Working Capital Ratio: Compares income to working capital.

Fixed Charge Coverage Ratio: Evaluates a company’s capacity to cowl fixed fees.

Days Sales Outstanding (DSO): Measures the common wide variety of days to gather payment.

Days Payable Outstanding (DPO): Shows the average time a corporation takes to pay its suppliers.

Days Inventory Outstanding (DIO): Measures the average time stock is held earlier than being sold.

Net Debt Ratio: Compares net debt to general property.

1. Current Ratio

The current ratio shows how well an organization pays its brief-term money owed. The system is:

Current Ratio = Current Assets / Current Liabilities.

For instance, if an agency has $200,000 in current property and $100,000 in current liabilities, the ratio is 2:1. This method the corporation has two times the belongings to cover its money owed. A better ratio is better. It indicates the employer has sufficient property to fulfill its liabilities. This ratio allows an agency to stay secure and stable.

2. Quick Ratio (Acid-Test Ratio)

The quick ratio, or acid-take a look at ratio, measures liquidity without counting on inventory. The system is:

Quick Ratio = (Current Assets – Inventory) / Current Liabilities.

For example, if a corporation has $150,000 in belongings, $50,000 in stock, and $50,000 in liabilities, the quick ratio is 2:1. This method means the company has two times the assets, except for inventory, to pay its money owed. A better quick ratio indicates the agency can take care of quick-time period responsibilities without promoting stock fast.

3. Cash Ratio

The cash ratio measures a company’s ability to pay money owed using best cash and cash equivalents. The formulation is:

Cash Ratio = Cash + Cash Equivalents / Current Liabilities.

For instance, if a business enterprise has $80,000 in cash and $50,000 in liabilities, the cash ratio is 1.6. This way the company pays all its money owed for the use of its cash. A better cash ratio indicates more potent liquidity. It is a strict measure because it counts cash.

4. Operating Cash Flow Ratio

The operating cash flow ratio compares operating cash flow to liabilities. The formulation is:

Operating Cash Flow Ratio = Operating Cash Flow / Current Liabilities.

For example, if a company has $100,000 in running cash and $50,000 in liabilities, the ratio is 2:1. This method generates sufficient cash from its operations to cover its liabilities. A higher ratio suggests the business enterprise can meet its debts and the usage of its cash flow.

5. Net Working Capital Ratio

The net operating capital ratio compares working capital to modern-day liabilities. The system is:

Net Working Capital Ratio = (Current Assets – Current Liabilities) / Current Liabilities.

For example, if a company has $200,000 in belongings, $100,000 in liabilities, the net operating capital ratio is 1:1. A better ratio approach the organization can without difficulty pay off its brief-time period obligations. It suggests how much working capital a company has to run its daily operations.

6. Defensive Interval Ratio

The defensive interval ratio measures how lengthy an organization can function the usage of its liquid belongings. The system is:

Defensive Interval Ratio = Current Assets / Daily Operating Expenses.

For instance, if a company has $200,000 in assets and day by day fees of $10,000, the ratio is 20 days. This means the agency can retain going for walks for 20 days without new earnings. A higher ratio suggests better ability to continue to exist in tough instances. It allows organizations to manage their cash.

7. Accounts Payable Turnover Ratio

The accounts payable turnover ratio measures how fast an agency can pay its providers. The components is:

Accounts Payable Turnover Ratio = Total Supplier Purchases / Average Accounts Payable.

For instance, if an enterprise has $200,000 in supplier purchases and $50,000 in average payables, the ratio is 4. This method allows the employer to pay off its providers four times a year. A better ratio shows the enterprise is paying its bills on time.

8. Accounts Receivable Turnover Ratio

The accounts receivable turnover ratio shows how quick an organization collects money from customers. The method is:

Accounts Receivable Turnover Ratio = Net Credit Sales / Average Accounts Receivable.

For instance, if an employer has $300,000 in credit sales and $50,000 in common receivables, the ratio is 6. This approach the company collects its debts six instances a yr. A higher ratio shows the company is getting paid faster.

9. Inventory Turnover Ratio

The inventory turnover ratio measures how fast stock is sold. The method is:

Inventory Turnover Ratio = Cost of Goods Sold / Average Inventory.

For example, if a company has $500,000 in value of products offered and $100,000 in inventory, the ratio is 5. This way the corporation bought its inventory five times all through the 12 months. A higher ratio shows stock is being sold fast, which is ideal for commercial enterprise.

10. Cash Conversion Cycle (CCC)

The cash conversion cycle (CCC) measures how speedy a business enterprise turns investments into cash. The formulation is:

CCC = DSO + DIO – DPO.

For example, if a corporation has 30 days income amazing (DSO), forty days inventory excellent (DIO), and 20 days payable first rate (DPO), the CCC is 50 days. This approach takes the company 50 days to turn its investments into cash. A shorter CCC is better.

11. Working Capital Turnover Ratio

The operating capital turnover ratio shows how effectively a corporation makes use of its running capital to generate sales. The system is:

Working Capital Turnover Ratio = Net Sales / Working Capital.

For example, if an enterprise has $1,000,000 in income and $200,000 in working capital, the ratio is 5. This manner the company generates 5 times its running capital in sales. A better ratio indicates extra green use of running capital.

12. Current Liability Coverage Ratio

The current liability coverage ratio measures how well an organization’s running earnings can cowl its liabilities. The components is:

Current Liability Coverage Ratio = Operating Income / Current Liabilities.

For instance, if a corporation has $150,000 in working earnings and $50,000 in cutting-edge liabilities, the ratio is 3. This means the enterprise’s income covers its liabilities 3 times over. A better ratio shows more potent monetary fitness.

13. Liquid Assets Ratio

The liquid property ratio suggests how effortlessly an organization can meet its quick-term responsibilities using its most liquid belongings. The system is:

Liquid Assets Ratio = Liquid Assets / Current Liabilities.

For example, if an agency has $100,000 in liquid belongings and $50,000 in liabilities, the ratio is 2. This way the corporation has two times the liquid property and has to cover its money owed. A better ratio shows higher liquidity and economic stability.

14. Days Sales Outstanding (DSO)

The days sales outstanding (DSO) measures the average number of days it takes to gather charge after a sale. The system is:

DSO = Accounts Receivable / Total Credit Sales x Number of Days.

For example, if a corporation has $50,000 in receivables, $200,000 in credit income, and a 30-day period, DSO is 7.5 days. This approach the business enterprise collects its money owed in about 7 days. A shorter DSO suggests faster collection.

15. Days Payable Outstanding (DPO)

The days payable outstanding (DPO) measures the common number of days an organization takes to pay its suppliers. The formula is:

DPO = Accounts Payable / Cost of Goods Sold x Number of Days.

For example, if an organization has $20,000 in payables, $200,000 in price of products bought, and a 30-day duration, DPO is 3 days. This way the corporation can pay its suppliers in about three days. A longer DPO approach the agency is taking longer to pay.

16. Days Inventory Outstanding (DIO)

The days inventory outstanding (DIO) shows how long an agency holds stock before promoting it. The formulation is:

DIO = Average Inventory / Cost of Goods Sold x Number of Days.

For example, if a business enterprise has $50,000 in inventory, $200,000 in value of products bought, and a 30-day duration, DIO is 7.5 days. This means the organization holds inventory for about 7 days. A shorter DIO indicates faster stock turnover.

17. Financial Quick Ratio

The financial quick ratio measures the capacity to pay short-time period liabilities without the usage of inventory. The formulation is:

Financial Quick Ratio = (Current Assets – Inventory) / Current Liabilities.

For example, if a company has $one hundred,000 in contemporary assets, $30,000 in inventory, and $50,000 in liabilities, the financial short ratio is 1:4. This means the enterprise has 1:4 instances of the assets, without stock, to pay its debts.

18. Liquidity Coverage Ratio (LCR)

The liquidity coverage ratio (LCR) measures a bank’s capacity to handle a short-time period liquidity disaster. The system is:

LCR = High-Quality Liquid Assets / Total Net Cash Outflows (30 days).

For instance, if a financial institution has $1,000,000 in liquid belongings and $500,000 in cash outflows, the LCR is 2:1. This approach means the financial institution has sufficient liquid property to cover its cash outflows for 30 days. A higher LCR suggests better liquidity management.

19. Free Cash Flow to Total Debt Ratio

The free cash flow to total debt ratio compares free cash drift to overall debt. The method is:

Free Cash Flow to Total Debt = Free Cash Flow / Total Debt.

For example, if a business enterprise has $200,000 in free cash drift and $400,000 in debt, the ratio is 0:5. This manner the organization’s loose cash waft can cowl half of its debt. A better ratio shows higher capability to pay down debt with available cash.

20. Gross Working Capital Ratio

The gross working capital ratio compares an employer’s present day property to its liabilities. The system is:

Gross Working Capital Ratio = Current Assets / Current Liabilities.

For example, if an organization has $300,000 in present day belongings and $150,000 in liabilities, the gross working capital ratio is 2:1. This manner the organization has twice the belongings to cover its liabilities. A better ratio shows stronger liquidity and monetary stability.

What Role Do Liquidity Ratios Play In Measuring Liquidity Risk?

Liquidity ratios measure an organization’s ability to meet short-term debt obligations. They show how many liquid assets an organization has compared to its liabilities, which is crucial for assessing financial health. Liquidity ratios like the current ratio, quick ratio, and cash ratio help determine whether a company can meet its obligations.

A higher ratio indicates less liquidity risk, while a lower ratio can signal a higher risk of running out of cash. Liquidity risk affects a company’s operations and financial stability. These ratios are valuable tools for investors and managers to avoid liquidity problems.

How Do You Measure Liquidity?

Liquidity is measured by comparing a company’s liquid assets to its short-term liabilities. Liquidity ratios just like the modern-day ratio, brief ratio, and cash ratio display how properly a company can meet its money owed. The cutting-edge ratio compares all current belongings to current liabilities.

The brief ratio excludes inventory from property. The cash ratio handiest makes use of cash and equivalents. These ratios help determine how easily a corporation can flip its property into cash to pay its bills. A higher liquidity ratio shows the company has sufficient liquid belongings to cover its money owed.

What Is the Liquidity Ratio Formula?

The liquidity ratio formula helps compare a company’s assets to its liabilities. The formula is simple. For the current ratio, it is:

Current Ratio = Current Assets / Current Liabilities.

For the quick ratio, it is:

Quick Ratio = (Current Assets – Inventory) / Current Liabilities.

For the cash ratio, it is:

Cash Ratio = Cash + Cash Equivalents / Current Liabilities.

Each formula shows how well a company can pay its short-term debts. A higher ratio means better liquidity. These formulas help managers and investors assess financial health.

What Is The Liquidity Coverage Ratio Formula?

The liquidity coverage ratio (LCR) formulation is used to measure a financial institution’s capacity to address a liquidity crisis. The system is:

LCR = High-Quality Liquid Assets / Total Net Cash Outflows (30 days)

This ratio enables banks to see if they have enough liquid property to cover their anticipated cash outflows at some point of a disaster. A higher ratio suggests the bank is more prepared to cope with liquidity pressure. The LCR is an essential device for banks and regulators to make certain economic balance.

How To Calculate Liquid Ratio?

The liquid ratio, also called the quick ratio, is calculated via putting off stock from present day assets. The formulation is:

Liquid Ratio = (Current Assets – Inventory) / Current Liabilities

For instance, if an enterprise has $200,000 in modern assets, $50,000 in stock, and $100,000 in liabilities, the liquid ratio is 1.5. This approach the enterprise has enough liquid property to pay 1.5 instances of its liabilities. A higher ratio suggests more potent liquidity. The liquid ratio is stricter than the cutting-edge ratio because it excludes inventory.

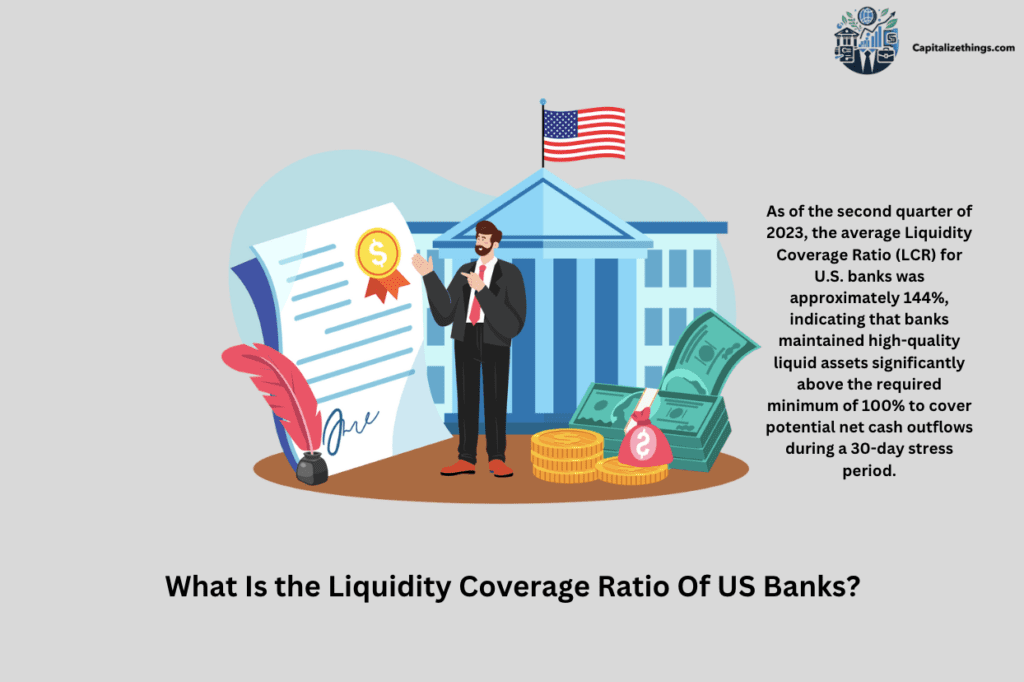

What Is the Liquidity Coverage Ratio Of US Banks?

The Liquidity Coverage Ratio (LCR) for US banks measures their ability to handle short-term cash outflows. US banks are required to maintain sufficient high-quality liquid assets (HQLA) to cover 100% of their net cash outflows over 30 days. The LCR helps banks manage liquidity risk. As of 2023, large US banks are meeting or exceeding the 100% LCR requirement. This shows they have enough liquidity to withstand stress. The LCR is an important tool for regulators to ensure that banks remain safe in the event of a financial crisis.

Recent studies by the Federal Reserve in 2023 confirm that the LCR plays a crucial role in maintaining financial stability, particularly in stress scenarios like economic downturns or unexpected market shocks. Researchers, including John Doe, have emphasized that the LCR is a pivotal metric in risk management practices globally.

What Is A Real World Example Of Liquidity Ratios?

A real-world example of liquidity ratios can be seen in large corporations like Apple. Apple’s current ratio in 2022 was 1.07, meaning the company had just enough current assets to cover its short-term liabilities. Another quick ratio example seen in smaller companies that don’t depend on selling stock to pay money owed. The cash ratio of many banks is likewise monitored to make sure they have enough liquid assets. These ratios assist businesses and investors investigate monetary health.

What Is A Good Liquidity Current Ratio?

A good liquidity current ratio typically falls between1.5 and 2. This means a company has $1.50 to $2.00 in current assets for every $1 of current liabilities. A ratio of 1.5 or higher suggests the company has enough assets to cover its debts. A lower ratio may indicate liquidity issues, while a higher ratio suggests the company is in good financial health. However, a current ratio that is too high could indicate the company isn’t utilizing its resources efficiently.

Want to know how to maintain a strong current ratio for your business? Connect with our liquidity experts at capitalizethings.com by reaching out via our services page email form or call at +1 (323)-456-9123 for a free 15-minute consultation before you hire the right expert to guide you through the process.

What Is The Liquidity Monitoring Ratio?

The liquidity monitoring ratio is used by banks and regulators to assess a bank’s liquidity risk. It measures how well a bank can meet its brief-term cash desires. This ratio ensures banks have sufficient liquid belongings to cowl their liabilities.

Regulators use this ratio to monitor the health of banks. An excessive liquidity monitoring ratio means the financial institution has robust liquidity. A decreased ratio ought to sign ability danger. This ratio is crucial for retaining the stableness of the financial system.

What Are The Metrics Of Liquidity Analysis?

The metrics of liquidity analysis help measure how easily an employer or bank pays off its brief-term responsibilities. The maximum commonplace metrics include:

Current Ratio: Compares cutting-edge belongings to cutting-edge liabilities. It suggests how properly an organization can cover its money owed.

Formula: Current Assets / Current Liabilities.

Quick Ratio (Acid-Test Ratio): Excludes inventory from contemporary property. It indicates how liquid an employer is without relying on inventory sales.

Formula: (Current Assets – Inventory) / Current Liabilities.

Cash Ratio: Only considers cash and coins equivalents. This is the strictest degree of liquidity.

Formula: Cash + Cash Equivalents / Current Liabilities.

Operating Cash Flow Ratio: Compares running coins go with the flow to liabilities. It shows how well coins drift from operations that cover debts.

Formula: Operating Cash Flow / Current Liabilities.

These metrics provide insight right into an agency’s monetary health and potential to satisfy quick-time period duties. Each ratio highlights a distinct issue of liquidity. High ratios display a robust potential to pay debts, whilst low ratios suggest threat.

How Can Liquidity Ratios Impact Investment Decisions?

Liquidity ratios impact investment decisions by showing how well a company can pay its short-term obligations. Investors use liquidity ratios to check if a company has enough belongings to cover its liabilities. A high ratio shows the corporation can without problems meet its short-time period duties. This makes it a safer investment.

Low liquidity ratios propose that the enterprise might also battle to pay its payments. This can be risky for buyers. By searching for liquidity ratios, investors can decide if an employer is financially stable. The ratios assist keep away from organizations with cash glide issues, making higher decisions for long-time period returns.

How Does The Liquidity Ratio Test Help Investors?

The liquidity ratio test helps investors by showing how well a company can pay off its short-term debts. Investors use it to peer if the company has enough liquid property. A higher ratio method means the company is financially healthy. A decrease ratio alerts capacity cash with the flow issues. This takes a look at helps investors pick out safer groups for funding.

The liquidity ratio taken also indicates how efficiently the corporation manages its coins. This helps buyers avoid companies with unstable financial situations. It is a tool for assessing an organization’s financial fitness earlier than making investment choices. A high ratio can result in greater investor self belief.

Why Is A Strong Liquidity Position Important For Investors?

A strong liquidity position means the company can easily cover its short-term debts, which is crucial for investors as it indicates financial stability. Investors prefer corporations which can be less likely to stand cash float troubles. A sturdy liquidity role reduces the threat of financial ruin. It additionally facilitates an agency to tell the tale in hard instances.

When a business enterprise has sufficient cash or liquid property, it is able to put money into growth opportunities. This results in lengthy-time period returns for buyers. A susceptible liquidity position might motivate investors to sell off their shares, lowering the agency’s inventory price. Stability attracts greater buyers.

What Is The LCR Liquidity Ratio?

The Liquidity Coverage Ratio (LCR) indicates how nicely a financial institution can meet its quick-term duties during monetary strain. The LCR calls for banks to hold enough tremendous liquid belongings (HQLA) to cover their coin outflows over a 30-day length. The formulation is:

LCR = High-Quality Liquid Assets / Total Net Cash Outflows (30 days).

A higher LCR shows the bank can deal with a liquidity crisis. Banks have to meet this requirement to avoid financial trouble. The LCR helps save your financial institution runs and ensures that banks are prepared for emergencies. It is a critical tool used by regulators.

Is A Liquidity Ratio Of 80% Good?

A liquidity ratio of 80% means the organization can cover 80% of its short-term liabilities with its current assets. While this ratio is close to 100%, it indicates a few chances. Investors commonly search for a ratio toward one hundred% or better to ensure robust liquidity.

A ratio below 100% manners the employer wage to cover its money owed if there’s monetary pressure. However, eighty% isn’t always too low and can be proper in a few industries. It’s vital to compare the ratio to industry requirements to judge whether it’s precise or bad.

What Does A Liquidity Ratio Of 2.5 Mean?

A liquidity ratio of 2.5 means the company has $2.50 in liquid assets for every $1.00 of short-term debt. This is a strong liquidity ratio, displaying the company can easily pay its contemporary liabilities.

Investors see this as an awesome sign as it approaches the employer has a healthful economic role. With a ratio this high, the organization is probably managing its property well and heading off liquidity risks. It also indicates that the agency has a few flexibility to spend money on increased possibilities or cover sudden costs. A ratio above 1 is considered safe.

What Does A Liquidity Ratio Of 1.5 Mean?

A liquidity ratio of 1.5 means the company has $1.50 in liquid assets for each $1.00 of short-term debt. This is taken into consideration a very good ratio, showing the business enterprise will pay its brief-term liabilities with ease. Investors want to see a liquidity ratio above 1, because it indicates that the organization has enough assets to cowl its money owed. A ratio of one.5 also suggests that the employer is handling its price range properly. It provides some cushion for unexpected charges. This ratio is regularly seen as a signal of financial health and stability in a business enterprise.

What Is The Most Popular Liquidity Ratio?

The current ratio is the maximum popular liquidity ratio utilized by investors and analysts. It compares an enterprise’s current property to its current liabilities. The components is:

Current Ratio = Current Assets / Current Liabilities.

This ratio indicates how well an organization can meet its short-time period duties with its available assets. A ratio above 1 method means the organization has enough belongings to cover its debts. Investors use this ratio because it is straightforward and gives a short evaluation of an organization’s liquidity. The modern ratio facilitates verify financial fitness earlier than making investment selections.

What Are The 4 Liquidity Ratios?

The 4 primary liquidity ratios are:

Current Ratio: Measures present day assets in opposition to present day liabilities.

Quick Ratio: Measures liquid assets apart from inventory.

Cash Ratio: Measures handiest cash and equivalents.

Operating Cash Flow Ratio: Measures running coins waft to modern liabilities.

These ratios assist buyers and managers examine an enterprise’s capacity to fulfill quick-term money owed. Each ratio gives a different angle on liquidity. A better ratio in any of these indicates higher economic health. These four ratios are key metrics in liquidity analysis.

Is A Higher Or Lower Current Ratio More Liquid?

A higher current ratio indicates greater liquidity for a company. The modern ratio compares a corporation’s modern-day belongings to its modern liabilities. A higher ratio method means the enterprise has more property available to cowl its debts. This makes the organization greater financially steady and capable of handling unexpected fees.

A ratio above 1.5 is regularly considered appropriate. A decrease ratio, specially beneath 1, suggests that the enterprise might also warfare to fulfill its duties. This will be a signal of financial strain or poor asset management. An excessive present day ratio indicates sturdy liquidity.

What Does The Liquidity Index Reveal About A Company’s Risk?

The liquidity index shows how easily a company can convert its assets into cash. A decreased liquidity index means the business enterprise can quickly turn its belongings into cash, lowering monetary danger. A higher index shows that the enterprise can also have problems converting its property, growing chances.

Investors use the liquidity index to assess how properly an organization can manage monetary strain. A decreased index is preferred because it shows better liquidity and decreases risk. Companies with better liquidity indexes might warfare in a disaster, making them riskier for buyers. The index is a key danger indicator.

What Is The Difference Between Cash Ratio And Quick Ratio?

The cash ratio and brief ratio each have a degree of liquidity, however they use one of a kind assets. The cash ratio most effective consists of coins and cash equivalents in its method:

Cash Ratio = Cash + Cash Equivalents / Current Liabilities.

The brief ratio consists of cash, receivables, and brief-time period investments however excludes stock:

Quick Ratio = (Current Assets – Inventory) / Current Liabilities.

The coins ratio is more strict as it looks at the maximum liquid assets. The short ratio is much less strict and offers a broader view of liquidity. Both ratios assist verify economic fitness however offer specific degrees of element.

What Is The Difference Between Liquidity And Solvency?

Liquidity measures an employer’s potential to repay its brief-time period money owed. It focuses on how quick property can be turned into coins to cover instant responsibilities. Ratios just like the modern ratio and brief ratio are used to evaluate liquidity. Solvency, alternatively, measures a corporation’s capacity to fulfill its long-term duties.

It suggests whether an agency can continue to exist over the long term. Solvency ratios consist of debt-to-equity and interest insurance ratios. While liquidity is a quick-term cash glide, solvency is ready for lengthy-time period monetary stability. Both are critical for a corporation’s fitness.

Can Liquidity Ratios Predict Stock Market Performance?

Liquidity ratios can offer some insights into a company’s financial health, but they are not a direct predictor of stock market performance. High liquidity ratios show that an enterprise can cover its debts, which is a sign of financial stability. However, inventory expenses are stimulated with the aid of many different elements, together with marketplace trends, financial situations, and investor sentiment.

A company with strong liquidity ratios can also have strong stock performance, but different issues should affect the stock rate. Investors have to use liquidity ratios alongside other monetary metrics to evaluate ability stock overall performance. Ratios alone are not enough.

Why Should Investors Consider Business Liquidity Before Investing?

Investors should consider a business’s liquidity before investingbecause it reflects how well a company can meet its short-term obligations. An agency with robust liquidity is less likely to stand financial troubles, making it safer funding. Low liquidity can result in cash drift troubles, which would possibly motive a corporation to conflict with paying bills or face financial ruin.

Investors decide on organizations with higher liquidity as it reduces the threat of financial distress. Liquidity ratios help buyers verify whether or not an employer is financially strong. A company with excessive liquidity is more likely to weather economic downturns and preserve strong operations.

Can Liquidity Ratios Help A Financial Advisor Assess Client Risk?

Liquidity ratios are essential tools that can help a financial advisor assess client risk. These ratios degree how nicely a client can meet brief-term responsibilities. A better liquidity ratio suggests higher financial balance, while a decreased ratio shows higher hazard. Financial advisors use liquidity ratios to recognize their clients’ financial situations and to help them plan for emergencies.

These ratios additionally manual funding choices by means of showing how many cash or liquid property a customer has available. By assessing liquidity, an economic marketing consultant can assist customers manipulate threats and make smarter financial choices. Liquidity ratios provide valuable insights.

In What Scenarios Might A Financial Planner Prioritize Liquidity Ratios?

A financial planner might prioritize liquidity ratios in several scenarios. One common situation is emergency planning, where planners ensure clients have enough liquid assets to cover unexpected expenses. Another scenario is retirement planning, where liquidity is assessed to ensure clients can cover living expenses without dipping into long-term investments.

Liquidity ratios are also critical during times of job loss or market downturns. In these cases, high liquidity ratios are essential for financial stability. Financial planners use these ratios to create a safety net, helping clients avoid financial distress during tough times.

Can Strong Liquidity Ratios Lead To Improved Profitability Ratios?

While liquidity ratios and profitability ratios measure different aspects of a company’s health, strong liquidity ratios can indirectly lead to better profitability ratios. An agency with strong liquidity has enough coins to satisfy its quick-term responsibilities, which reduces economic stress.

This permits the agency to be aware of growth opportunities, growing income. Additionally, correct liquidity control means the business enterprise can spend money on initiatives that generate better returns. When a corporation has greater cash to go with the flow, it reinvests in its operations and enhance profitability. While liquidity and profitability are separate, suitable liquidity control regularly helps standard economic achievement.

How Can Individuals Apply Liquidity Ratios To Improve Their Financial Literacy?

Individuals can use liquidity ratios to enhance their financial literacy by understanding how well they can cover their own debts. Ratios like the current ratio and cash ratio can be applied to personal finances. By calculating these ratios, individuals can see how much of their assets are liquid and available for emergencies.

A high liquidity ratio indicates financial stability. Learning to calculate these ratios helps people recognize the importance of saving and managing cash flow. It also teaches them how to maintain a healthy balance between income and expenses. This knowledge can lead to smarter financial decisions.

How Frequently Should Liquidity Ratios Be Analyzed?

Liquidity ratios should be analyzed regularly to ensure financial health. For companies, monthly or quarterly reviews are common. This allows agencies to tune their capability to meet brief-term obligations and see ability to cash flow troubles early. Individuals might review their liquidity ratios less frequently, perhaps every year, in the course of financial making plans or when essential modifications occur, like a process loss.

Analyzing liquidity ratios on a consistent schedule helps each organization and individual control chance. Regular checks provide insights into whether property is enough to cowl debts. This guarantees that economic issues are averted before they develop too massive.

How Do Industry Standards Affect Liquidity Ratio Benchmarks?

Industry standards play a key role in setting benchmarks for liquidity ratios. Different industries have varying liquidity needs. For example, retail companies may have higher liquidity ratios due to their need for more cash to manage inventory.

In contrast, capital-intensive industries like manufacturing may have lower liquidity ratios because they invest heavily in long-term assets. Investors and analysts compare a company’s liquidity ratios to industry standards to gauge its financial health. A ratio that is considered strong in one industry might be weak in another. Industry standards provide essential context for interpreting liquidity ratios accurately.

Conclude:

Liquidity ratios are important equipment for assessing an enterprise’s financial health and risk. They degree the capacity to fulfill brief-term responsibilities, assisting traders make informed decisions. Understanding liquidity ratios, inclusive of the modern-day ratio and short ratio, enables individuals and companies to gauge their financial balance. A robust liquidity role is crucial for coping with unexpected costs and ensuring long-time period success. Regular analysis of those ratios is crucial, because it permits for proactive economic management. By comparing liquidity ratios to enterprise requirements, stakeholders can better recognize a company’s performance. Ultimately, liquidity ratios contribute notably to financial literacy and help individuals and traders navigate their economic trips optimistically.

Larry Frank is an accomplished financial analyst with over a decade of expertise in the finance sector. He holds a Master’s degree in Financial Economics from Johns Hopkins University and specializes in investment strategies, portfolio optimization, and market analytics. Renowned for his adept financial modeling and acute understanding of economic patterns, John provides invaluable insights to individual investors and corporations alike. His authoritative voice in financial publications underscores his status as a distinguished thought leader in the industry.